The Economic Effects of Bulgaria’s Eurozone Accession

The Economic Effects

of Bulgaria’s Eurozone Accession*

Abstract

Bulgaria is set to adopt the euro on 1 January 2026. This paper asks a simple but consequential question: what will actually change, and for whom? To answer it, the analysis draws on comparative evidence from Slovakia, Slovenia, Croatia, and the Baltic states, countries that joined the Eurozone over the past two decades under broadly similar conditions, alongside recent macroeconomic data from official sources. The goal is not to produce a verdict for or against the euro, but to map the likely effects as clearly as the available evidence allows. The central argument is cautious. Euro adoption is unlikely to trigger an immediate economic boom. What it can do is act as an institutional anchor — one that strengthens policy credibility, compresses risk premia, and improves the conditions for long-term convergence. Whether these gains materialize depends less on the currency itself than on what Bulgaria does with the framework it is entering: fiscal discipline, governance quality, and institutional capacity will matter more than the exchange rate ever did. The paper also takes the risks seriously. Political instability, demographic decline, and structural weaknesses do not disappear at the moment of accession. In some respects, the euro makes them more consequential, not less.

Keywords

Economics, Optimum Currency Area, Eurozone Accession, Economic Convergence, Bulgaria.

I. Introduction

Since its accession to the European Union in 2007, Bulgaria has been formally committed to adopting the euro. For many years, however, this commitment remained mostly symbolic. Despite the existence of a currency board since 1997 and the fixed exchange rate of 1.95583 BGN per euro, political instability, public skepticism, and institutional weakness repeatedly delayed real progress toward Eurozone membership.1

Bulgaria’s entry into the Exchange Rate Mechanism II (ERM II) in 2020 marked a turning point. For the first time, euro adoption moved from a distant political objective to a realistic economic process. Despite several changes of governments and ongoing political tensions, 1 January 2026 is today confirmed as the target date by both Bulgarian authorities and European institutions.2,3,4,5

At the same time, Bulgarian society remains deeply divided on the issue. For some, the euro represents stability, integration, and protection from future crises. For others, it is seen as a loss of sovereignty and a threat to national control over economic life. Much of this debate is driven by political emotions rather than economic reasoning, which makes a structured, evidence-based analysis necessary.6,7,8

What makes Bulgaria’s case particularly distinctive is its monetary history. Unlike most post-socialist countries that entered the Eurozone from a position of formal monetary sovereignty, Bulgaria has operated under a currency board since 1997, a regime introduced after a severe financial and hyperinflationary crisis that destroyed public trust in the national currency. Under this system, the Bulgarian National Bank has no independent monetary policy: interest rates are close to the euro rates, and the lev is fixed irrevocably to the euro at 1.95583. In this sense, Bulgaria has already lived under the core discipline of a monetary union for nearly three decades. Euro adoption is therefore the institutional completion of a regime that has de facto existed since 1997.9,10,11

This paper addresses the following research question: To what extent is Bulgaria’s euro adoption likely to support long-term economic convergence in terms of GDP growth, inflation stability, and investment inflows, and what specific short-term risks, such as inflation spikes and interest rate changes, does it involve?

The paper proceeds as follows. Section II introduces the theoretical framework of Optimum Currency Area theory and its application to Bulgaria. Section III describes the methodology. Section IV presents and discusses the results, covering Bulgaria’s macroeconomic position, the potential risks, the potential benefits, and the role of the currency board as a pre-euro regime. Section V concludes and identifies directions for future research.

II. Theoretical Framework

To understand what euro adoption could mean for Bulgaria, it is necessary to briefly introduce the main ideas from the economic theory of currency unions.

The classical starting point is the Optimum Currency Area (OCA) theory, first developed by Robert Mundell in 1961.12 Mundell argued that countries benefit from sharing a common currency when they have strong economic integration, such as high labor mobility, capital mobility, and mechanisms for absorbing regional economic shocks.

Later economists expanded this idea. Economist Ronald McKinnon emphasized that small and open economies, where a large part of production is traded internationally, are better candidates for a common currency.13,14 Augmenting this research, economist Peter Kenen added that countries with diversified economies suffer less from sector-specific shocks and are therefore more suitable for monetary unions.15

Together, these ideas form the core of classical currency union theory. According to this framework, adopting a common currency involves an important trade-off:

• Countries lose control over their own monetary policy (interest rates and exchange rates).16

• In return, they gain lower transaction costs, price transparency, and deeper financial integration.17

Whether this trade-off is beneficial depends on the structure of the economy and the quality of institutions.

Modern approaches go beyond purely technical economics and underline that monetary unions are also political and institutional projects. As economist Peter Verdun argues, the euro is not only a currency, but a form of shared governance that reshapes national economic decision-making.18

The Belgian economist Paul De Grauwe also stresses that a monetary union can function well only if it is supported by strong institutions and effective economic coordination. Without this, countries may become vulnerable to asymmetric shocks and financial crises even inside a common currency area.19

III. Methodology

To analyze the potential effects of Bulgaria’s euro adoption, this paper combines three complementary approaches: comparative analysis, macroeconomic data analysis, and an event-study perspective. The goal is to connect economic theory with real-world evidence in a way that is structured, transparent, and suitable for a student-level academic study.

Comparative Country Analysis

The first method is a comparative analysis between Bulgaria and several countries that adopted the euro in the past two decades: Slovakia, Slovenia, Croatia and the Baltic states.

These countries were selected because they share important similarities with Bulgaria:

• They are small and open economies.

• They underwent a post-socialist economic transition.

• They are strongly integrated into EU trade.

• They adopted the euro after a period of structural reforms.

The comparison is not meant to predict Bulgaria’s trajectory, but the patterns that emerge across these cases, as shifts in inflation, changes in investment flows, movements in interest rates are too consistent to ignore.20,21.

However, the study does not assume that Bulgaria will simply repeat these countries’ experiences. Instead, these countries are treated as reference cases that help identify likely tendencies and potential risks, not as exact models.

Macroeconomic Data Analysis

The second method is a quantitative analysis of Bulgaria’s recent macroeconomic performance, focusing on five indicators: real GDP growth, inflation, unemployment, public debt, and foreign direct investment.

These indicators are examined for the period 2020–2025 to capture recent economic trends and the post-pandemic environment.

Data are taken from internationally recognized and reliable sources, including IMF country reports, Eurostat databases, and World Bank statistics22,23. These sources ensure that the analysis is based on comparable and consistent data.

Event-Study Approach

To analyze the short-term effects of euro adoption, the paper also uses an event-study approach.

This approach focuses on what happens around the time when a country adopts the euro. It examines economic changes before, during, and after the adoption moment. In this study, attention is given to:

• inflation behavior around the changeover

• changes in capital inflows

• shifts in borrowing costs and financial risk perception

The event-study method helps isolate changes that are closely related in time to euro adoption, while separating them from longer-term global trends.22

Limitations of the Methodology

Like any academic study, this research has important limitations.

First, Bulgaria’s situation in 2026 will not be identical to that of any country that adopted the euro in the past. Global conditions, geopolitical risks, and technological changes create a different environment.

Second, macroeconomic data cannot capture all social and political factors, such as public trust, institutional quality, or political stability, which strongly influence economic outcomes.

Third, correlations in data do not automatically imply causation. Even if changes occur around euro adoption, they may be influenced by other factors such as global markets or domestic structural reforms.22

Despite these limitations, the chosen methodology provides a balanced and structured way to analyze Bulgaria’s euro adoption. It combines theory, data, and comparative experience, which is appropriate for a mature student-level academic study.

IV. Results and Discussion

Macroeconomic Context of Bulgaria before Euro Adoption

Economic growth

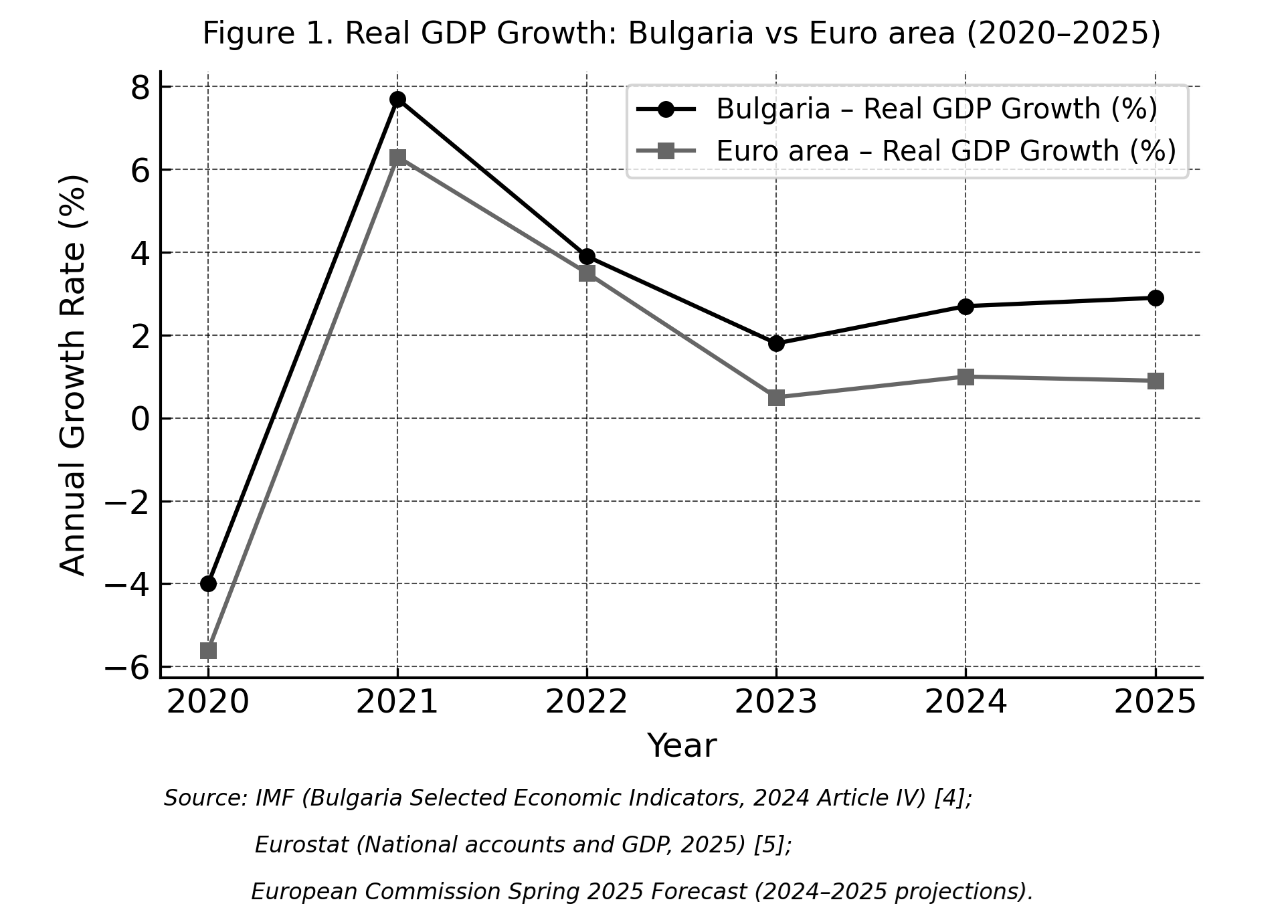

Figure 1 compares real GDP growth in Bulgaria and the euro area between 2020 and 2025.

Figure 1. Real GDP growth: Bulgaria vs Euro area (2020–2025). The figure shows that Bulgaria experienced a stronger post-pandemic rebound than the euro area and maintained higher growth rates in most years. However, Bulgaria’s growth path is more volatile, reflecting the greater sensitivity of small open economies to external shocks.

Bulgaria experienced a strong post-pandemic rebound in 2021, with real GDP growth close to 8%, higher than the euro area average for the same year24,25,26. Although growth slowed afterwards, Bulgaria has remained consistently above the euro area average between 2023 and 2025. This suggests that, at least in terms of growth performance, Bulgaria is not entering the Eurozone as a weak or stagnating economy, but as one that has recently outperformed the European average.

At the same time, the data also shows higher volatility. While the euro area follows a more stable trend, Bulgaria’s growth path fluctuates more sharply. This is typical for smaller, open economies that are more exposed to external shocks, such as energy or food price changes or shifts in global demand.

This volatility is important when thinking about euro adoption, because joining the euro could reduce some sources of instability, especially exchange rate uncertainty and risk premia.

Inflation

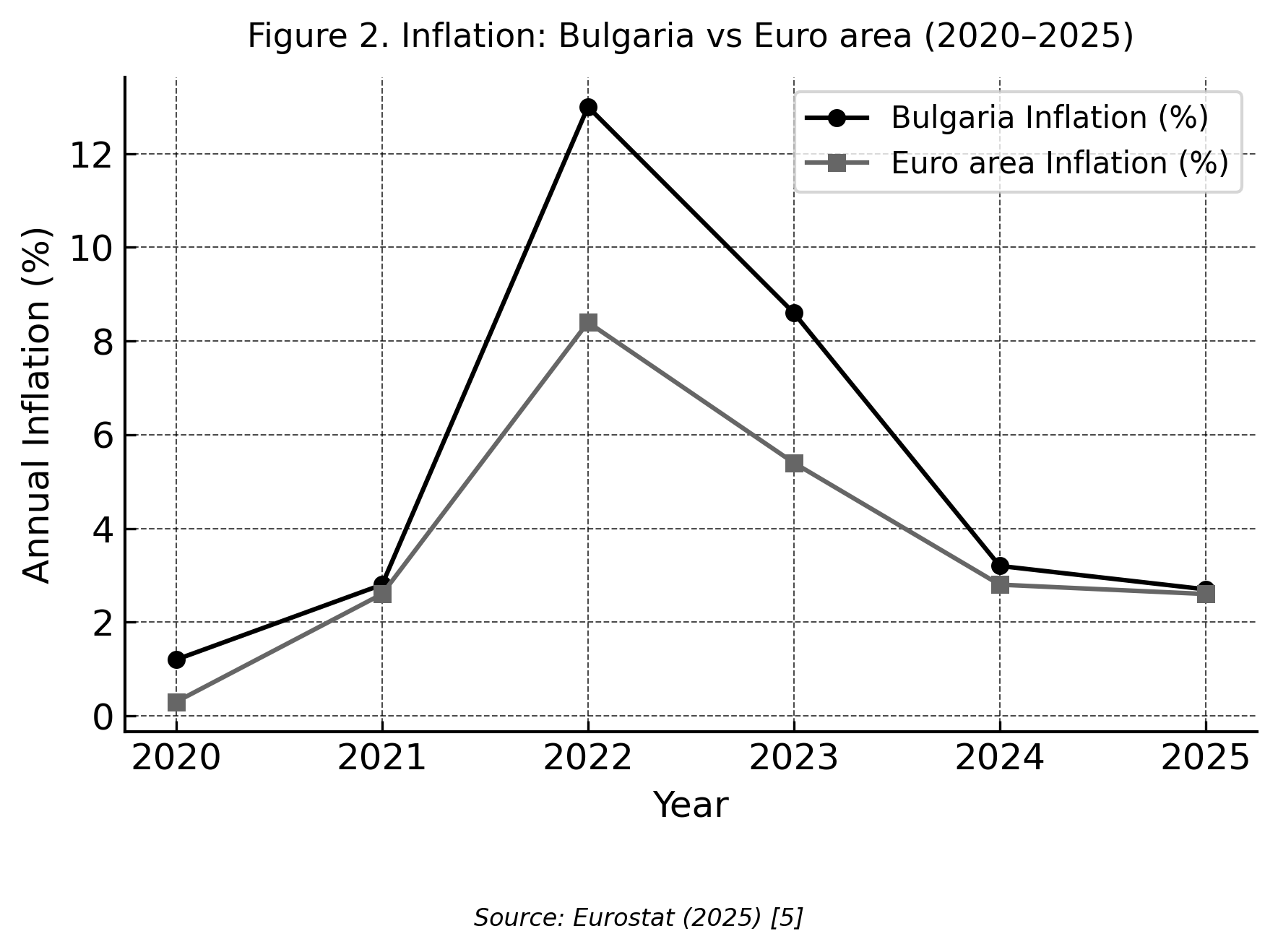

Inflation is one of the most sensitive topics in the public debate on euro adoption.

Figure 2. Inflation: Bulgaria vs Euro area (2020–2025). The figure illustrates that Bulgaria recorded significantly higher inflation than the euro area during the 2022–2023 shock period. At its peak, Bulgarian inflation exceeded 13%, while euro area inflation peaked at around 8–9%27,28.

This difference is often used as an argument against adopting the euro. However, an important point is that this inflation surge happened without the euro. It was mainly driven by external factors (energy prices, supply chain disruptions) and internal ones, such as market structures, regulation, and price-setting behavior, a rapid increase in salaries and pensions, and growing state budget expenses.

In fact, countries with stronger institutions and more disciplined fiscal policies absorbed the same shock with considerably lower inflation — suggesting that Bulgaria’s vulnerability lies not in its currency, but in how domestic structures transmit and amplify external pressures. The practical implication for the transition is straightforward: the greater risk is not euro-induced inflation, but insufficient capacity to prevent opportunistic price rounding during the changeover, which depends on whether Bulgarian institutions are strong enough to prevent price abuses and opportunistic rounding during the transition.

Labor market

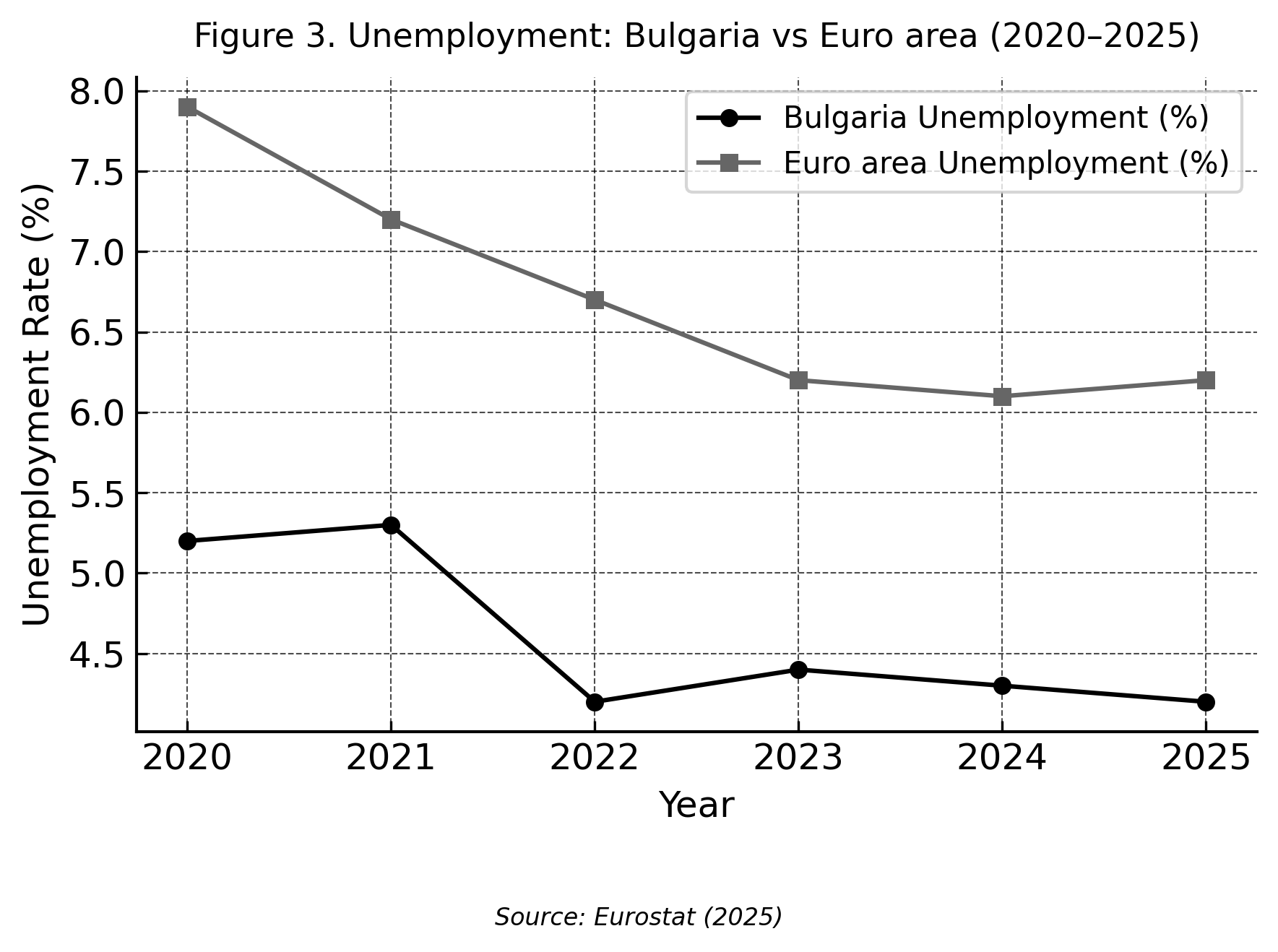

Figure 3 shows unemployment rates for Bulgaria and the euro area.

Figure 3. Unemployment: Bulgaria vs Euro area (2020–2025). The figure shows that Bulgaria’s unemployment rate remained consistently below the euro area average throughout the period. This indicates relatively strong labor market conditions despite broader macroeconomic volatility.

Interestingly, Bulgaria’s unemployment rate has stayed consistently below the euro area average throughout the period. In 2022–2025, it fluctuates around 4.2–4.4%, compared to approximately 6–7% for the euro area20,26.

Employment levels are relatively strong and stable. Structural problems exist, especially demographic decline and emigration, but these are long-term issues and are not directly caused by currency choice.29,30

From this perspective, adopting the euro is unlikely to create a large shock to employment. The more relevant question is whether it can indirectly improve labor market quality through higher investment, productivity, and wage convergence.

Public debt and fiscal position

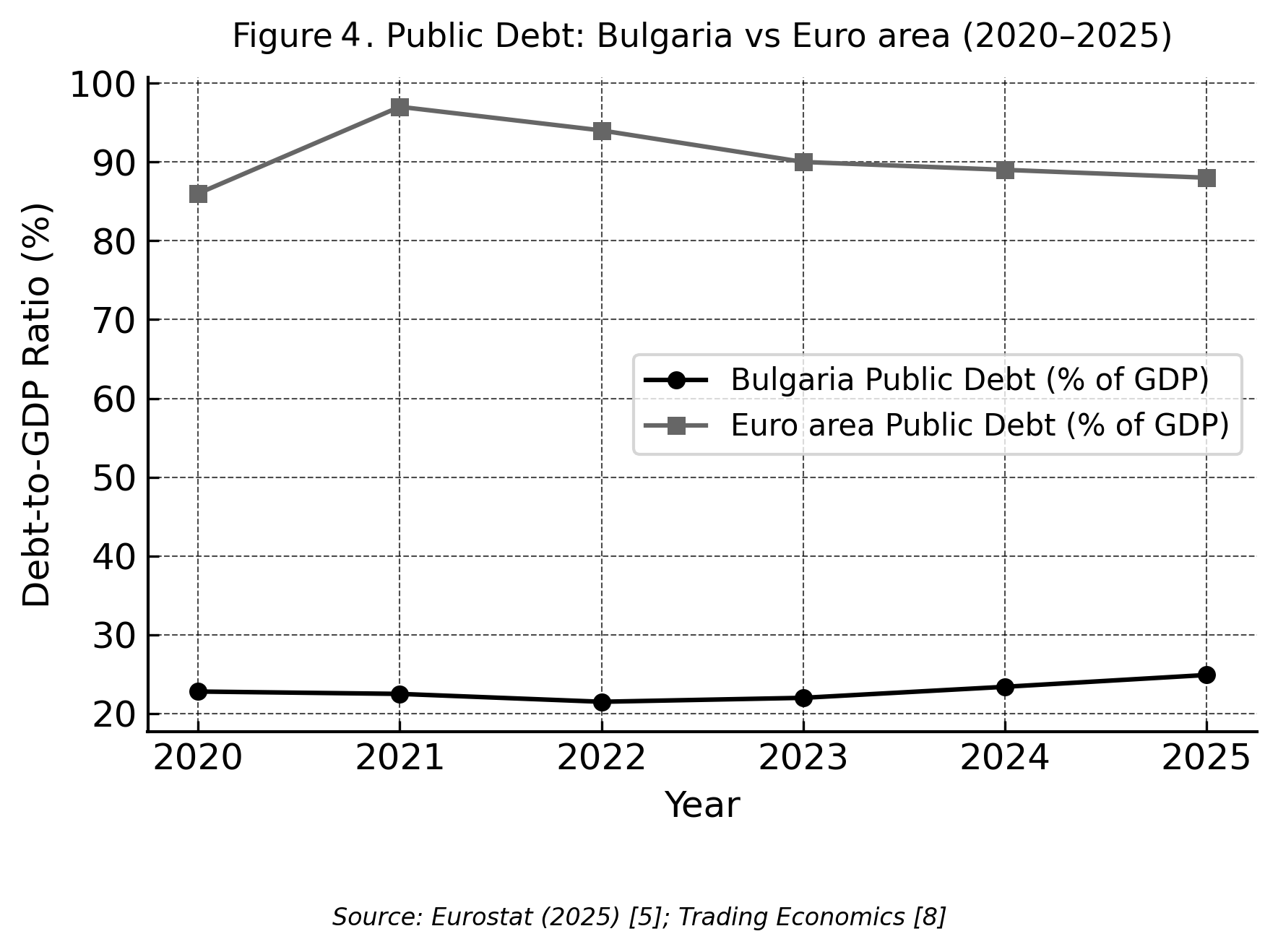

One of Bulgaria’s strongest arguments for Eurozone membership is its public debt.

As shown in Figure 4, Bulgaria’s government debt remains very low, around 22–25% of GDP in the 2020–2025 period, compared to nearly 90% for the euro area average22,31.

Figure 4. Public debt: Bulgaria vs Euro area (2020–2025). The figure highlights Bulgaria’s exceptionally low public debt compared to the euro area average. This provides Bulgaria with substantial fiscal space and represents a key macroeconomic strength ahead of euro adoption.

This is a major structural advantage. It means that Bulgaria enters the euro with relatively strong fiscal space and lower vulnerability to debt crises. Historically, countries like Greece or Italy entered the Eurozone with much higher debt levels and weaker fiscal discipline, which contributed to later instability.

High debt is not inherently dangerous — Japan has maintained an enormous public debt for decades while remaining a prosperous economy. The real risk arises when debt is combined with weak institutions and low investor confidence, as the Greek crisis a decade ago demonstrated.

However, low debt does not automatically guarantee long-term stability. Political instability and repeated elections in the last three years have sometimes delayed budget adoption, reforms, and fiscal planning. If this continues, Bulgaria risks undermining one of its main strengths just as it enters the Eurozone.

Foreign direct investment

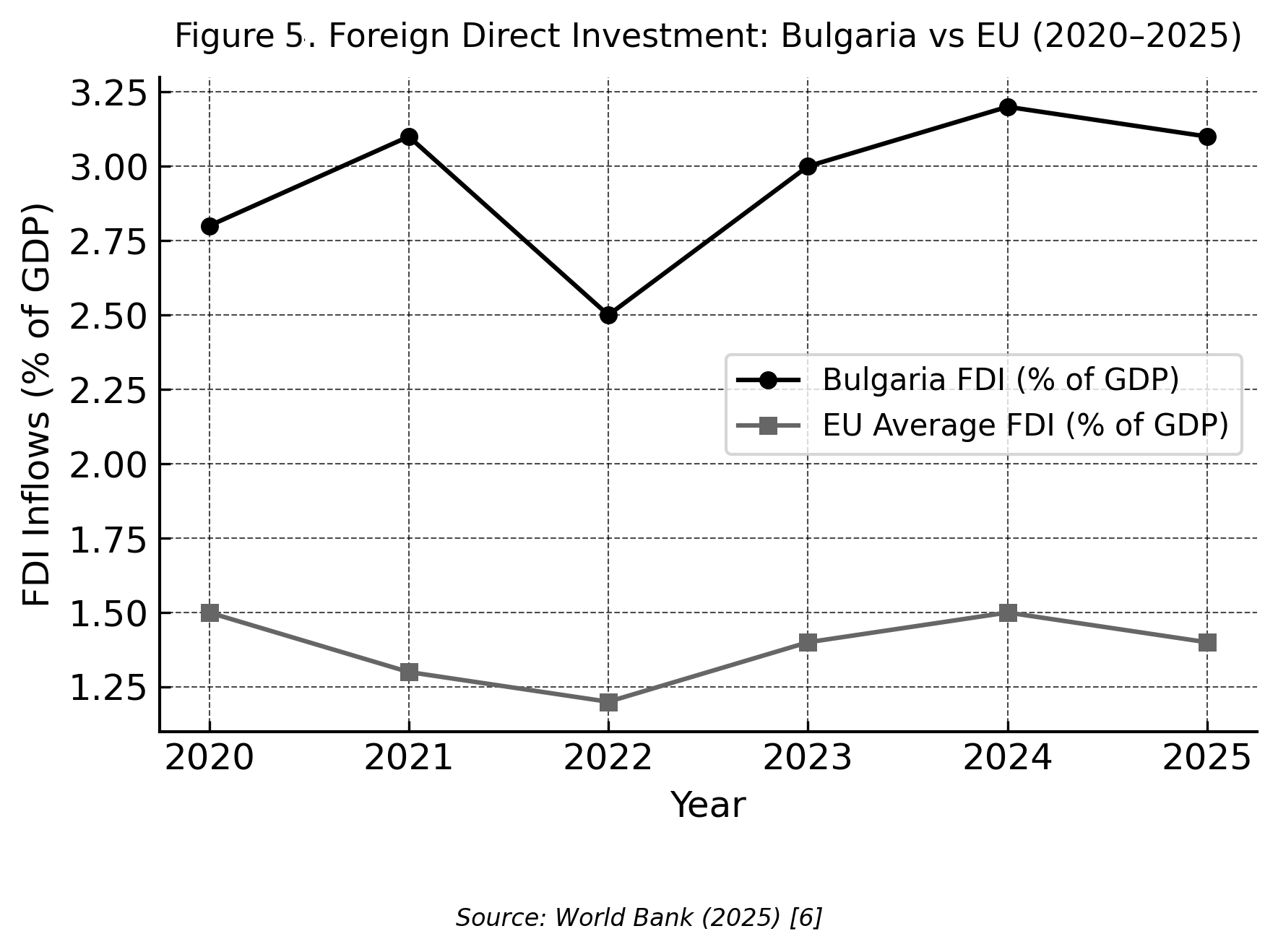

Finally, Figure 5 shows foreign direct investment inflows as a share of GDP.

Figure 5. Foreign direct investment: Bulgaria vs EU (2020–2025). The figure shows that Bulgaria attracted higher FDI inflows relative to GDP than the EU average over the period. This indicates strong investor interest even prior to euro adoption, reflecting favorable structural and cost conditions.

Bulgaria consistently attracts higher FDI relative to its economic size than the EU average, with inflows around 2.5–3.2% of GDP, compared to around 1.2–1.5% for the EU.22

The above indicates that Bulgaria is already seen as an attractive destination for foreign capital, even before adopting the euro. Lower labor costs, lower taxes, EU membership, and geographic position all play a role here.

Based on experiences from other countries, euro adoption could further increase investor confidence by removing currency risk and improving financial integration.20 But these gains are not automatic. Investors also care about legal stability, corruption levels, infrastructure, and administrative efficiency.32

If euro adoption is not accompanied by institutional improvements, the initial FDI boost may be short-lived.

Potential Risks and Costs of Euro Adoption for Bulgaria

Euro adoption is often presented as a net positive process, but its risks are real and should not be underestimated. For Bulgaria, some of the most important risks are concentrated around inflation expectations, short-term interest rate changes, distributional and social effects, and political perception. This section does not argue against euro adoption. Instead, it shows why the transition must be managed carefully.

Short-term inflation and price effects

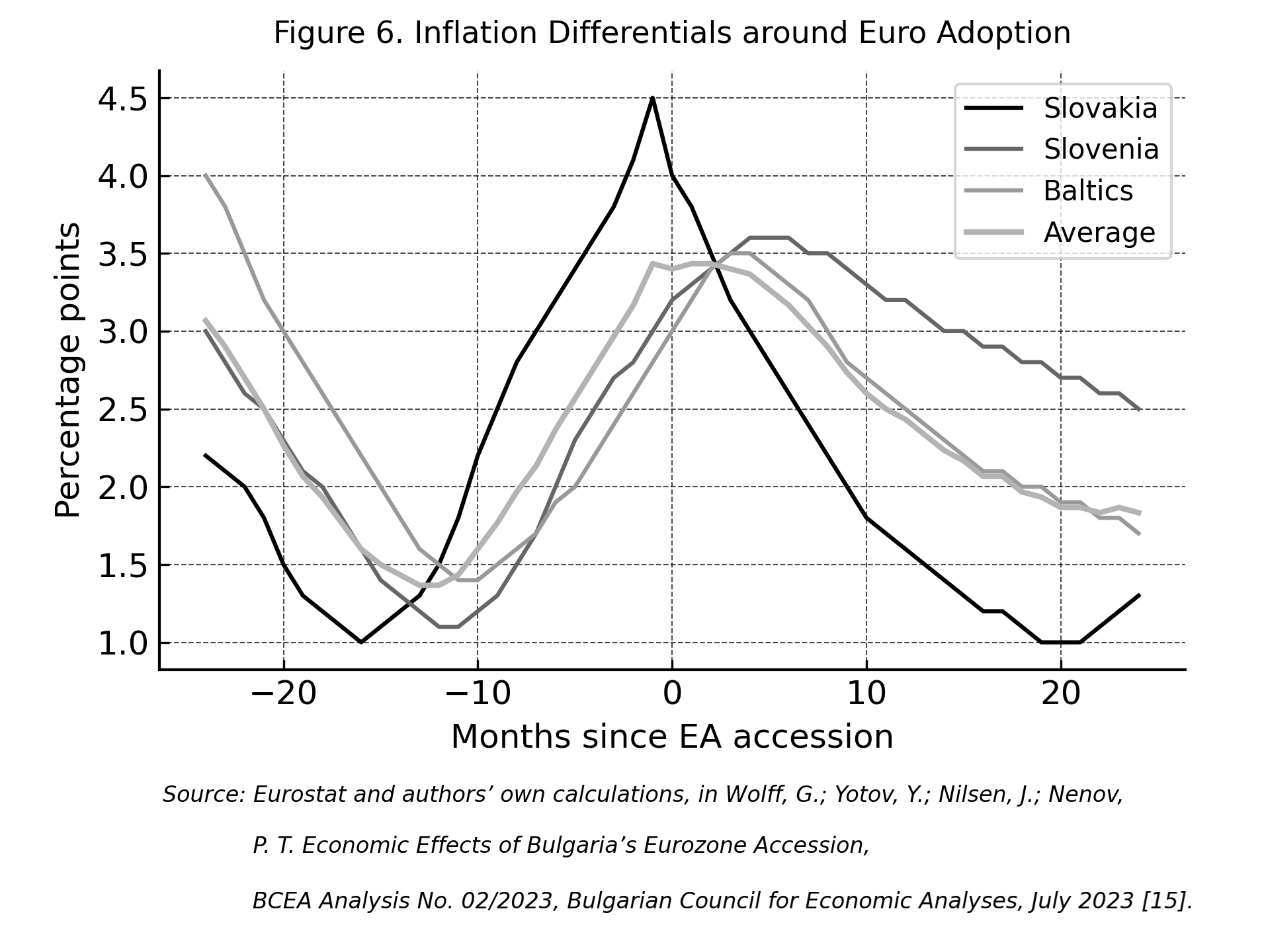

One of the strongest public fears is that prices will rise because of the euro.

Figure 6 shows inflation patterns around euro adoption in countries like Slovakia, Slovenia, and the Baltic states.

Figure 6. Inflation differentials around euro adoption. The figure shows a temporary increase in inflation around the euro changeover period, particularly in the months immediately following adoption. This effect is short-lived and tends to stabilize over time, suggesting that euro adoption is associated with modest transitional price pressures rather than persistent inflation.

It suggests that inflation tends to increase slightly around the changeover period, especially in the service sector, before gradually stabilizing20,33. The change of the currency itself does not cause the increase. Price rounding during conversion, opportunistic behavior by some firms, and heightened inflation expectations among consumers all play a role — effects that are modest in aggregate but can feel acute for low-income households, for whom a 2--3% rise in food, transport, and local services is far more visible than movements in GDP or FDI.

If the government fails to communicate clearly and enforce price transparency, this short-term effect can damage public trust in the entire process.

Short-term increase in interest rates on loans

A risk that receives considerably less public attention concerns interest rates on private loans, particularly mortgages. Bulgarian borrowers currently enjoy unusually low rates — deposits near zero, lending rates around 3% — a product of the domestic banking market’s specific structure rather than any deliberate policy choice. After euro adoption, lending conditions will gradually align more closely with euro area money market rates, especially the Euribor benchmark.34

At the moment, average mortgage interest rates in Bulgaria are around 2.5%34, which is significantly lower than in many Eurozone countries. After adopting the euro, as Bulgarian banks integrate more directly into the euro money market, these rates could move closer to euro area levels, which currently stand nearer to 4–4.5%.

For households with variable-rate mortgages, this is not an abstraction. A loan with a monthly repayment of 500 EUR could easily increase to 700–800 EUR over a relatively short period.

This carries several risks:

• increased financial pressure on middle-income households

• higher probability of loan defaults for vulnerable borrowers35

• cooling of the real estate market and construction sector

While higher rates can reduce speculative bubbles and improve long-term financial stability, the short-term social and political effects of such an adjustment could be significant, especially if wages do not grow at the same pace.

Loss of limited monetary flexibility

A second commonly mentioned risk is the loss of independent monetary policy.

In theory, when a country adopts the euro, it will no longer be able to control its own interest rates or exchange rate. These policies will be decided by the European Central Bank, based on the average conditions in the whole Eurozone.

In the Bulgarian case, however, the classical argument about the “loss of monetary sovereignty” needs to be reconsidered. In practice, Bulgaria surrendered that sovereignty in 1997 when it adopted the currency board and it is not obvious that anyone has seriously suffered from it since.

The real risk lies elsewhere. If Bulgaria’s economic cycle differs significantly from the euro area cycle, ECB policies may not always fit Bulgaria’s needs. For example:

• If Bulgaria enters a recession while the euro area grows, ECB monetary policy may be too tight.

• If Bulgaria overheats while the euro area stagnates, policy may be too loose.28,36

This creates vulnerability to so-called asymmetric shocks.

Uneven distribution of costs

The costs of euro adoption will not affect everyone equally.

• Borrowers with variable-rate loans (the majority of Bulgarian borrowers) will be more exposed to higher interest rates.

• Pensioners and low-income households will feel price changes more strongly.

• Exporters and firms integrated into European markets may benefit more quickly.

This uneven distribution of effects creates political tension. Even if the overall economy benefits in the long term, certain groups may feel that they are “paying the price” in the short term.

If this social dimension is ignored, support for euro adoption could collapse after entry, as happened in some Southern European countries after the financial crisis.

Political and institutional risks

Bulgaria’s repeated elections, unstable governments, and polarization have already affected its image and credibility in the eyes of investors and European partners.22

If euro adoption happens in a context of institutional weakness, poor communication, and lack of political consensus, the process itself could deepen distrust instead of strengthening integration.

In this sense, the biggest risk may not be economic, but institutional and political.

Potential Benefits of Euro Adoption for Bulgaria

Supporters of Bulgaria’s entry into the Eurozone often present it as an unavoidable step “towards Europe”, but this argument is too abstract. The real question is not whether the euro is a symbol of integration, but what concrete economic benefits it could bring to Bulgaria.

This section focuses on four of the most important potential benefits: lower risk and borrowing costs, higher investment and capital inflows, stronger institutional anchoring, and deeper economic integration.

Lower risk premia and borrowing costs

One of the most direct economic benefits of euro adoption is the reduction of currency risk.

At the moment, Bulgaria operates under a currency board with a fixed exchange rate to the euro, which already limits exchange rate volatility. However, for international investors, Bulgarian assets still carry “currency risk” because the BGN is technically a different currency. This risk increases borrowing costs for both the government and the private sector.

By adopting the euro, Bulgaria would eliminate this risk. This should lead to:

• lower government bond yields

• lower interest rates on corporate and private loans (in the longer term)

• lower mortgage rates for households (again in the longer term)

Empirical evidence from other Central and Eastern European countries shows that sovereign bond spreads typically compress after euro adoption.20 This happens because markets treat eurozone members as less risky in currency terms, even if they still differentiate between stronger and weaker economies.

We should have in mind that this benefit depends on future fiscal discipline. If Bulgaria weakens its public finances after joining, the credibility gains could quickly disappear, as seen in some Southern European countries after 2008.37

Higher foreign investment and capital inflows

Another frequently mentioned benefit is the potential increase in foreign direct investment and capital inflows.

As shown in Figure 5, Bulgaria already attracts relatively strong FDI inflows compared to the EU average. This suggests that investors already see potential in the country.

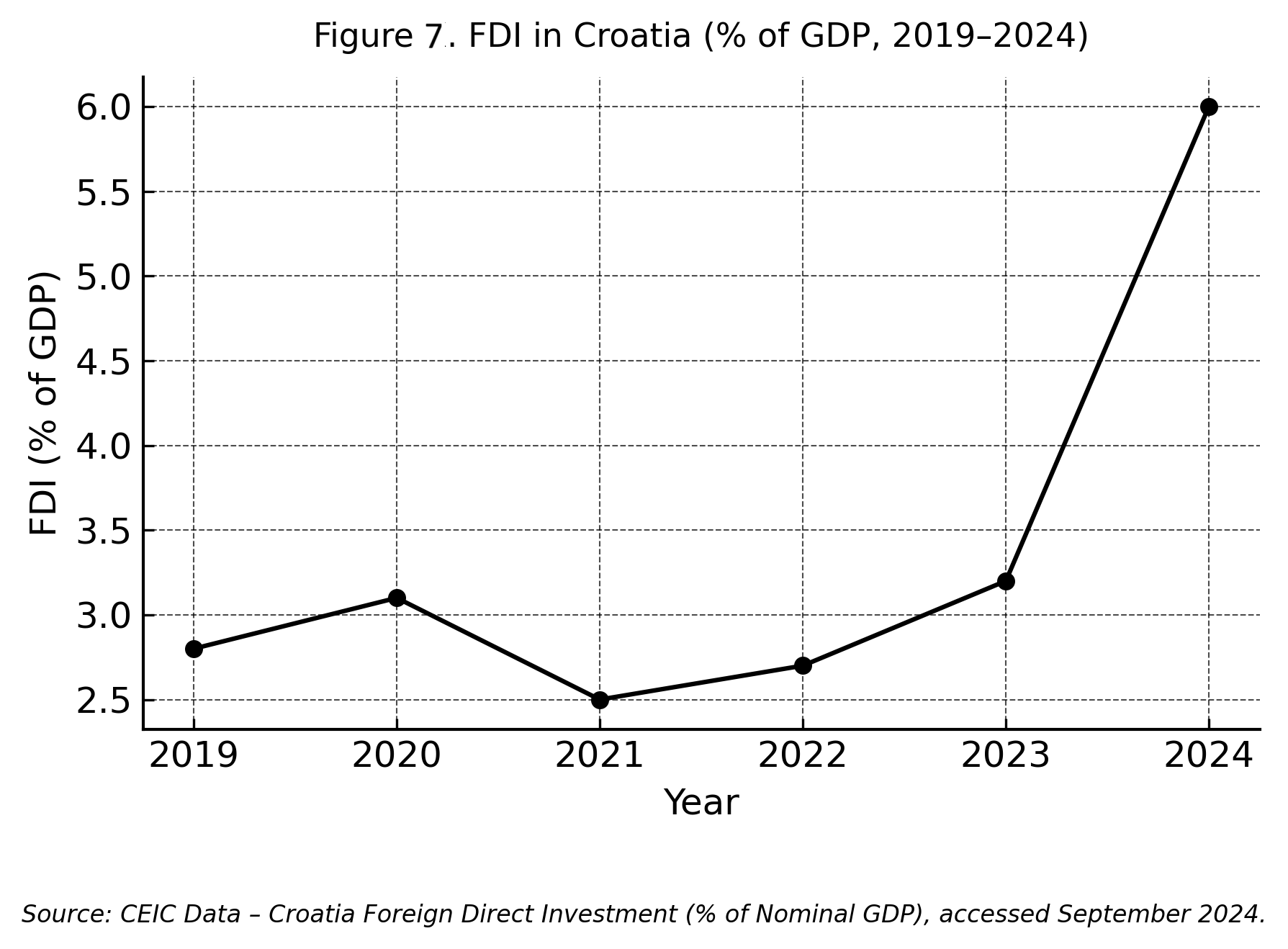

Figure 7 illustrates the post-adoption dynamics of foreign direct investment in Croatia. It shows a visible increase in net inflows in the period following euro entry, coinciding with improved investor confidence and stronger integration into the European financial space20,22,38.

Figure 7. Foreign direct investment inflows after euro adoption: the case of Croatia. The figure illustrates a noticeable increase in net foreign direct investment inflows following euro adoption. This pattern suggests that euro entry can act as a credibility signal that temporarily strengthens investor confidence before inflows normalize.

This suggests that euro adoption can act as an additional credibility signal, especially for countries from South-Eastern Europe that still suffer from a perception of political and institutional risk.

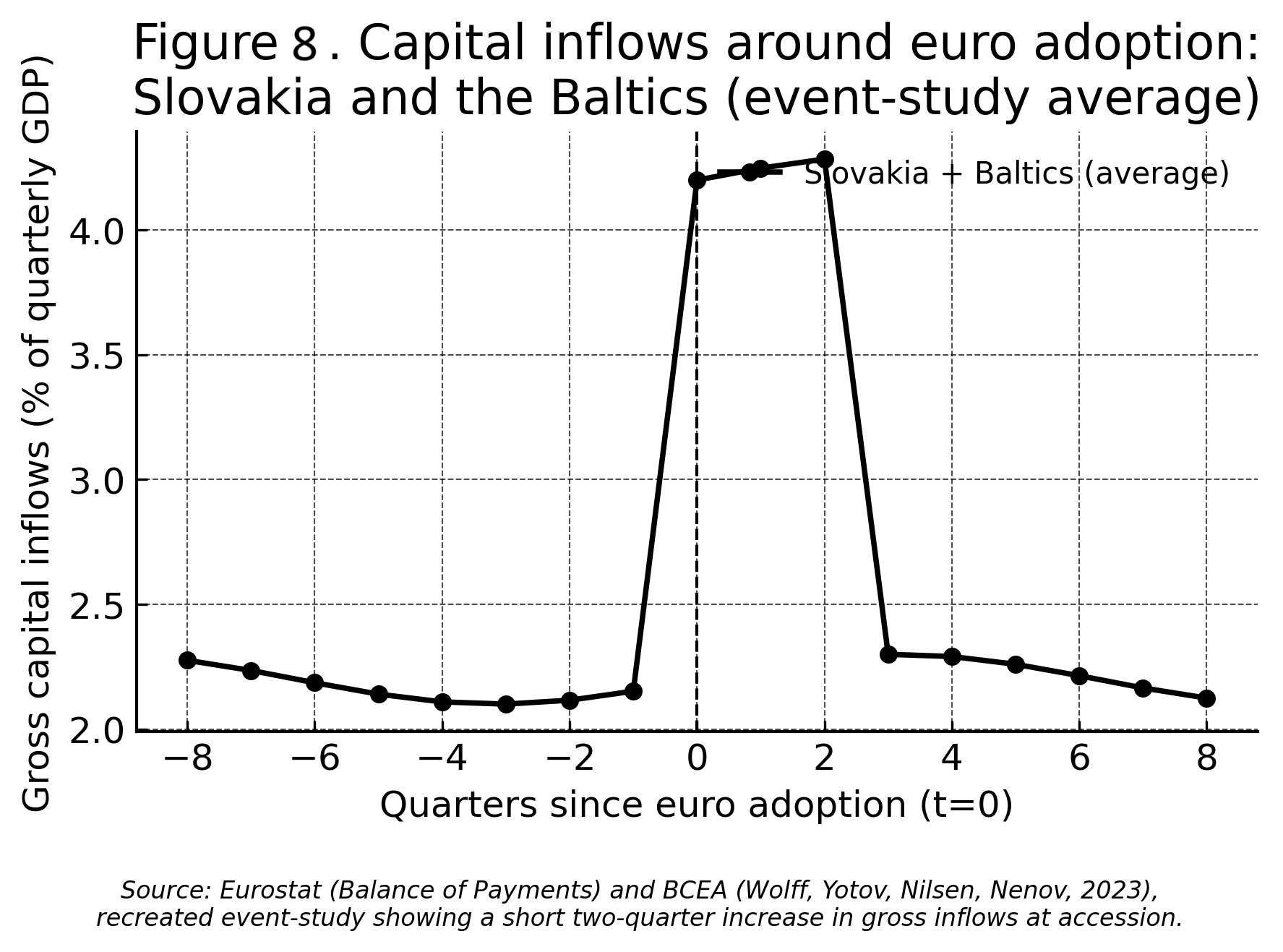

Figure 8 illustrates this effect using an event-study for Slovakia and the Baltic states.

Figure 8. Capital inflows around euro adoption in Slovakia and the Baltic states. The figure shows a clear short-term surge in capital inflows around the moment of euro adoption, followed by a gradual normalization. This pattern indicates that euro entry tends to generate temporary confidence-driven inflows rather than a permanent increase in capital.

This suggests two important points:

• Euro adoption can generate a temporary wave of capital inflows.

• This effect is often strongest around the adoption year, rather than permanently high afterwards.

For Bulgaria, this could mean a surge in investment in sectors such as real estate, software programming, and financial services. But if not properly managed, rapid capital inflows can also create asset price bubbles, which is why regulatory capacity and financial supervision become even more important after joining the euro.

Institutional anchoring and credibility

Joining the Eurozone means entering a framework with stricter fiscal rules, closer monitoring, and deeper integration into European decision-making structures, including the European Central Bank and the European Stability Mechanism20,31.

For a country like Bulgaria, which struggles with political instability and weak institutional trust, this can act as an external anchor. It does not magically improve governance, but it increases the cost of irresponsible policies and enhances external pressure for stability and reforms. The transfer of the largest Bulgarian banks under the direct control of the ECB also means significantly stricter rules and financial discipline in lending.

Deeper integration and long-term convergence

Removing currency barriers reduces transaction costs, simplifies trade, and improves price transparency — effects that matter particularly for a small open economy whose growth depends heavily on EU markets. Data from the Baltic states and Slovakia show that euro adoption was followed by a gradual increase in financial integration, export activity, and participation in European production networks.20,39

But convergence is not automatic, and the euro is not a shortcut. Closing the income gap with Western Europe still requires progress on education and human capital, infrastructure, digitalization, and institutional quality. Without movement on these fronts, membership in the common currency area will not by itself do the work.

Monetary Stability and the Currency Board as a Pre-Euro Regime

Since 1997, Bulgaria has operated under a currency board — a regime introduced in the aftermath of a severe financial and hyperinflationary crisis that had effectively destroyed public trust in the national currency. Under this arrangement, the lev is fixed irrevocably to the euro and the Bulgarian National Bank has no independent monetary policy to speak of. This arrangement brought long-term stability after a period of hyperinflation and financial collapse.10,11,40

This stability, however, comes at a structural cost: under a currency board, the central bank must hold sufficient foreign reserves to cover the entire money supply. This means that monetary expansion depends directly on the inflow of foreign currency into the country.

The Bulgarian currency board should not be interpreted merely as a stabilization mechanism of the 1990s, but as a long-term substitute for euro membership. In this sense, the euro does not replace the currency board: it completes and institutionalizes it. Bulgaria enters the Eurozone not from monetary independence, but from a system of externally anchored monetary discipline.

Currency Swap

By 2025, Bulgaria’s foreign exchange reserves will be around 40.6 billion euros, of which approximately 28–30 billion euros are liquid assets. At the same time, the money supply (M1) in Bulgaria exceeds 137 billion Bulgarian lev28 (approximately 70 billion EUR).

This means that not all money in circulation is covered by fully liquid reserves. In normal conditions, this is not a problem because not everyone exchanges their money at the same time. However, in theory, this creates vulnerability in extreme situations, such as a sudden loss of confidence in the banking system.

Euro adoption will fundamentally change this situation.

During the changeover process, the European Central Bank provides the euro banknotes and electronic liquidity needed to replace all Bulgarian levs in circulation. In exchange, the BGN is withdrawn, and Bulgaria’s existing foreign reserves, gold holdings, and international positions are integrated into the balance sheet of the Eurosystem.

In practical terms, this means that the limitation of Bulgaria’s own reserves suddenly disappears. Every lev in circulation will be converted into euros at the fixed rate of 1.95583, without Bulgaria needing to borrow externally or face a balance of payments crisis.

In effect, Bulgaria surrenders all its foreign reserves to the Eurosystem, but receives in return more than twice the value in euro liquidity. Whatever its political dimensions, this is unambiguously an increase in the country’s monetary wealth.

So, beyond the political and symbolic meaning of joining the euro, there is also a very technical but important effect:

Bulgaria moves from a national system with limited reserves to being part of a much larger monetary system with almost unlimited euro liquidity support.

This significantly reduces the risk of a classical currency crisis like the one experienced in 1996–1997, where the national currency collapses due to loss of reserves. On the other hand, it significantly strengthens long-term monetary stability and reduces the risk of a liquidity panic or speculative attack on the currency - something that small open economies with their own currencies are always vulnerable to.

However, euro adoption does not eliminate all risks. It transforms them. Currency risk disappears, but risks related to fiscal stability, banking sector stability, and economic competitiveness remain.

Currency Crises vs. Eurozone Crises

There is an important difference between:

• a currency crisis (collapse of the national currency), and

• a Eurozone-type crisis (debt or banking crisis within the common currency)

By adopting the euro, Bulgaria removes the possibility of a currency collapse and sharp devaluation, which is important for long-term stability and investor confidence.

However, countries like Greece, Spain, and Ireland have shown that it is still possible to experience deep economic and financial crises inside the Eurozone. The difference is that these crises are not caused by exchange rate instability, but by problems such as excessive debt, banking fragility, or weak institutions.37

This shows again that euro adoption is not a magic solution. It removes some risks while exposing the country more strongly to others.

Participation in Eurozone rescue mechanisms

After joining the Eurozone, Bulgaria will become part of the European Stability Mechanism (ESM), a fund designed to support member states in serious financial distress.41

As a result, Bulgaria may be required to contribute financially to rescue packages for heavily indebted countries such as Italy, Greece, or others in the event of a new debt crisis. To make this concrete: in a hypothetical debt crisis involving a country the size of Italy, Bulgaria’s contribution to cover even one third of the affected debt could reach approximately 660 million euros.

From an economic perspective, Bulgaria’s contribution would likely be limited in size, given the country’s relatively small share in Eurozone GDP. But from a social and political perspective, this issue is far more sensitive.

Bulgaria currently has one of the lowest public debt levels in the European Union, while several Eurozone countries operate with debt ratios above 130–150% of GDP.21 For many Bulgarian citizens, the idea that a relatively poor country with disciplined public finances might help finance bailouts for richer but more indebted economies is deeply controversial.

This creates a perception of unfairness, regardless of the technical details.

Even though similar arguments were used in Germany, the Netherlands, and Finland during the Greek debt crisis, they resonate even more strongly in Bulgaria due to its lower income levels and widespread distrust in European institutions. This risk is therefore not only financial, but also psychological and political. If a future Eurozone crisis occurs soon after Bulgaria joins, and if public communication is weak, this issue could significantly undermine public support for the euro and fuel euroscepticism.34

Certainly, the ESM would also support Bulgaria in case of a crisis like any other Eurozone state, but given the low level of Bulgaria’s public debt, such a scenario is highly unlikely.

V. Conclusion and Directions for Future Research

Bulgaria’s planned adoption of the euro represents a major turning point in the country’s economic development. It is not simply a technical change of currency, but a long-term institutional and macroeconomic transformation that will influence the way the economy functions for decades.

The main argument of this paper is that euro adoption should be seen as a framework for future development, not as an automatic solution to Bulgaria’s economic problems.

A key finding of this study is that Bulgaria’s euro adoption differs fundamentally from that of other CEE countries due to its long-standing currency board regime.

Bulgaria enters the euro from a position of relative macroeconomic strength. Public debt is low, growth has recovered, and the banking system is stable. However, these strengths are weakened by political instability and institutional problems.

The short-term risks of euro adoption are real. These include temporary inflation effects, potential mismatches between Bulgaria’s economic cycle and ECB policies, and social tensions related to price perceptions and increased interest rates on loans and mortgages.

The long-term benefits of euro adoption are significant. Lower transaction costs, reduced currency risk, potentially higher foreign investment, and stronger institutional discipline may support Bulgaria’s economic convergence with the rest of the European Union. However, these benefits will only materialize if Bulgaria continues to improve its institutions and governance.

Finally, euro adoption does not so much improve Bulgaria’s monetary stability as transform it. The nationally constrained currency board gives way to participation in a monetary framework of an entirely different scale — one that eliminates the risk of currency collapse, but makes fiscal discipline and institutional strength more consequential than ever.

Several directions remain open for future research. The distributional effects of euro adoption — how the transition affects different income groups and social layers — deserve more granular analysis than macroeconomic aggregates can provide.42 Sector-level studies would also be valuable: manufacturing, tourism, and logistics each face the changeover under different conditions, and their responses are likely to diverge. Perhaps most importantly, the relationship between public trust and institutional performance warrants closer attention. The economics of euro adoption are, in the end, only part of the story.

Acknowledgments

I would like to thank Dr. Iva Bimpli for her mentorship throughout the process of writing this research paper. Her guidance in structuring the research, analyzing the data, and critically engaging with the comparative literature was invaluable in shaping both the methodology and the conclusions of this study.

References

1. Nenovsky, N., Hristov, K., Petrova, I. & Petrov, B. “The Currency Board in Bulgaria: Design, Peculiarities and Management of Foreign Exchange Cover.” Bulgarian National Bank Discussion Papers, DP/9/1999. Sofia: Bulgarian National Bank, 1999.

2. European Central Bank. Bulgaria and the Euro: Progress and Challenges. Frankfurt: ECB Publications, 2023.

3. European Central Bank. “Communiqué on Bulgaria.” Press Release, 10 July 2020. Available at: ecb.europa.eu

4. Dorrucci, E., Fidora, M., Gartner, C. & Zumer, T. “The European Exchange Rate Mechanism (ERM II) as a Preparatory Phase on the Path towards Euro Adoption – The Cases of Bulgaria and Croatia.” ECB Economic Bulletin, No. 8, 2021. European Central Bank, Frankfurt.

5. Schadler, S. (ed.). Euro Adoption in Central and Eastern Europe: Opportunities and Challenges. Washington, D.C.: International Monetary Fund, 2005.

6. Atkinson, A. B. Inequality: What Can Be Done? Cambridge, MA: Harvard University Press, 2015.

7. Shiller, R. J. Narrative Economics: How Stories Go Viral and Drive Major Economic Events. Princeton: Princeton University Press, 2019.

8. Krastev, I. After Europe. Philadelphia: University of Pennsylvania Press, 2017.

9. Campos, N. F. & Coricelli, F. “Financial Liberalization and Democracy: The Role of Reform Reversals.” Open Economies Review, Vol. 23, No. 3, 2012, pp. 443–462.

10. Berlemann, M. & Nenovsky, N. “Lending of First versus Lending of Last Resort: The Bulgarian Financial Crisis of 1996/1997.” Comparative Economic Studies, Vol. 46, No. 2, 2004, pp. 245–271.

11. Enoch, C. & Gulde, A.-M. “Are Currency Boards a Cure for All Monetary Problems?” Finance & Development, Vol. 35, No. 4, 1998, pp. 40–43.

12. Mundell, R. “A Theory of Optimum Currency Areas”. American Economic Review, Vol. 51, No. 4, 1961, pp. 657–665.

13. McKinnon, R. “Optimum Currency Areas”. American Economic Review, Vol. 53, No. 4, 1963, pp. 717–725.

14. Kenen, P. The Theory of Optimum Currency Areas: An Eclectic View. Chicago: University of Chicago Press, 1969.

15. Frankel, J. & Rose, A. “The Endogeneity of the Optimum Currency Area Criteria”. Economic Journal, Vol. 108, No. 449, 1998, pp. 1009–1025.

16. Eurostat. Labour Force Survey. Luxembourg: European Commission, 2024. Available at: ec.europa.eu/Eurostat.

17. North, D. C. Institutions, Institutional Change and Economic Performance. Cambridge: Cambridge University Press, 1990.

18. Verdun, A. “A Historical Institutionalist Explanation of the EU’s Responses to the Euro Area Financial Crisis.” Journal of European Public Policy, Vol. 22, No. 2, 2015, pp. 219–237.

19. De Grauwe, P. Economics of Monetary Union, 13th ed. Oxford: Oxford University Press, 2021.

20. Bussière, M., Fidrmuc, J. & Schnatz, B. “Trade Integration of Central and Eastern European Countries: Lessons from a Gravity Model.” ECB Working Paper, No. 545. Frankfurt: European Central Bank, 2005.

21. IMF. Bulgaria: 2024 Article IV Consultation. IMF Country Report No. 24/117. Washington, D.C.: International Monetary Fund, 2024.

22. World Bank. World Development Indicators. Washington, D.C.: World Bank, 2023.

23. IMF. World Economic Outlook Database. Washington, D.C.: International Monetary Fund, October 2024.

24. Baldwin, R. & Wyplosz, C. The Economics of European Integration, 6th ed. New York: McGraw-Hill, 2019.

25. Wolff, G., Yotov, Y., Nilsen, J. & Nenov, P. T., et al. Euro Adoption in CEE. BCEA Working Paper 23/07. Brussels: BCEA, 2023.

26. Eurostat. Labour Market Statistics at Regional Level. Luxembourg: European Commission, 2024. Available at: https://ec.europa.eu/eurostat/statistics-explained/index.php/Labour_market_statistics_at_regional_level

27. Acemoglu, D. & Robinson, J. Why Nations Fail: The Origins of Power, Prosperity, and Poverty. New York: Crown, 2012.

28. Bulgarian National Bank. Economic Review, 2/2025. Sofia: BNB, 2025. Available at: https://www.bnb.bg/bnbweb/groups/public/documents/bnb_publication/pub_ec_r_2025_02_en.pdf

29. National Statistical Institute of Bulgaria. Population and Demographic Processes 2023. Sofia: NSI, 2024. Available at: nsi.bg

30. OECD. OECD Economic Surveys: Bulgaria. Paris: OECD Publishing, 2023.

31. Rose, A. K. “One Money, One Market: The Effect of Common Currencies on Trade”. Economic Policy, Vol. 15, No. 30, 2000, pp. 8–45.

32. European Commission. Convergence Report 2025. Brussels: European Commission, 2025.

33. Eurostat. Harmonised Indices of Consumer Prices (HICP). Luxembourg: European Commission, 2025. Available at: ec.europa.eu/eurostat

34. BTA :: Central Bank: November Mortgage Rates Stay Under 2.5%. https://www.bta.bg/en/news/economy/1035243-central-bank-november-mortgage-rates-stay-under-2-5-

35. Campbell, J. Y. “Household Finance”. Journal of Finance, Vol. 61, No. 4, 2006, pp. 1553–1604.

36. De Grauwe, P. & Ji, Y. “Flexibility versus Stability: A Difficult Trade-off in the Eurozone.” CEPR Discussion Paper No. DP11372. London: Centre for Economic Policy Research, 2016.

37. Gorton, G. Slapped by the Invisible Hand: The Panic of 2007. New York: Oxford University Press, 2010.

38. IMF. Croatia: 2023 Article IV Consultation. IMF Staff Country Report No. 23/233. Washington, D.C.: International Monetary Fund, 2023.

39. Eichengreen, B. The European Economy since 1945: Coordinated Capitalism and Beyond. Princeton: Princeton University Press, 2007.

40. Alesina, A. & Barro, R. J. “Currency Unions”. Quarterly Journal of Economics, Vol. 117, No. 2, 2002, pp. 409–436.

41. European Stability Mechanism. ESM Guidebook. Luxembourg: European Stability Mechanism, 2022. Available at: esm.europa.eu

42. European Commission. Standard Eurobarometer 102 — Autumn 2024. Brussels: European Commission, 2024. Available at: europa.eu/eurobarometer

*This article is published in the International Journal of High School Research, Vol. 8, Issue 9 (May 2026), pp. 255-263.

Issue: https://ijhsr.terrajournals.org/vol-8-issue9.html

DOI: https://doi.org/10.36838/IJHSR89.255